Helping clients decide on the best place to age, and how to afford it, is foundational planning. When done correctly, it's the most invaluable planning decision for all generations.

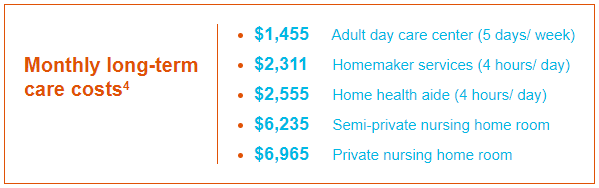

As you look toward retirement, you’ve likely worked hard to build a life you’re proud of — and the last thing you want is for an unexpected health event to unravel the security you’ve created. You’re not alone in that concern. The reality is that nearly 70% of people turning 65 today will need some form of long-term care at some point, and Medicare typically does not cover those costs.

This is one of the most emotionally charged financial conversations families face. No parent wants to feel like a burden to their children, and no adult child wants to watch a parent struggle to access the care they deserve. These are deeply human fears, and they’re entirely understandable.

What makes long-term care planning so important is how quickly circumstances can change. Whether due to illness, cognitive decline, or simply the natural progression of aging, the need for help with daily activities or medical care can arise suddenly and without warning. In fact, roughly half of all Americans will take on a caregiving role for a loved one at some point in their lives — a responsibility that touches every aspect of life, from personal finances to family relationships to emotional well-being.

The good news is that thoughtful, proactive planning can make an enormous difference. With the right strategies in place — including long-term care insurance and a comprehensive financial plan — you can preserve your independence, protect your family from financial hardship, and ensure that when care is needed, the focus remains where it belongs: on health and quality of life, not on how to pay for it.

So where do you begin? Let’s explore the options available to you and your family.

So what are your options as you begin to think ahead to how you’ll pay for the care you or your parents might need?

Discussing signs of aging or declining health can be an uncomfortable but important conversation to have with a loved one.

Discussing long-term care insurance is the most loving and important financial conversation you will ever have.

"I have Medicare, I don't need to plan for long-term care."

The unfortunate reality is that Medicare will only pay for a nursing home in very limited circumstances. According to Medicare policies, the insurance program will pay nursing home charges under these conditions:

the care is considered medically necessary;

the facility care is only needed for a limited period of time;

the care is provided by a Medicare-certified, skilled facility that is qualified to provide rehabilitation therapies; and,

the patient enters the nursing home after a qualifying inpatient hospital stay of three days or more.

These restrictions make it difficult for elderly people to qualify for nursing home care under Medicare. In condition three, for instance, the facility must be designed to manage, observe, or treat your medical needs after a hospitalization. Therefore, the more traditional nursing homes that provide day-to-day, non-medical care are not covered by Medicare.

What do you plan to do? To be financially prepared to cover the cost of a long-term care event for yourself?

Active lifestyle

Aging Seniors in Good Health

Concerned About the Risk

Energy professionals

Who Needs Long-Term Care?

It is difficult to predict what sort of long-term care an individual might need or for how long care may be required. Several factors increase the risk of needing long-term care.

Age the risk of a care need generally increases as people grow older, today many of us are are living well into our 90s.

Gender Women are at higher risk than men, primarily because they often live longer or have been a care provider for another.

Marital status Single people are more likely than married people to wish care from a paid provider.

Lifestyle Poor diet and exercise habits can increase an individual’s risk.

Health and medical history these factors also affect risk and can make it tougher to aquire coverage.

Profession career path can increase an individual’s risk, particularly physically demanding fields such as oil field service, Military, Police & Fire, or professional athlete.

Business Partners of Different Ages

Senior Caregivers

Retired Athletes

When Preserving Assets

As an independent insurance provider, Cavalry offers state partnership plans, stand-alone long-term policies (cover home health, assisted living, and nursing homes), and hybrid life and long-term care insurance policies.

Available policy types, optional riders, and applicable discounts will vary depending on the carrier and the policyholder’s health status, but will typically include the above-mentioned coverages as well as group products and tax-qualified plans, riders like inflation protection and return of premium, and discounts for spouses and household members.

Thanks for stopping in.

Thanks for stopping in.{kind=link}